People walk past a garden featuring a sign of the Forum on China-Africa Cooperation (FOCAC) on 31 August 2024. AFP.

China's August PMI data indicates the current headwinds to growth are continuing. Despite the rate cuts earlier this year, Chief Economist Mansoor Mohi-uddin maintains that more support is necessary for China's flagging financial markets.

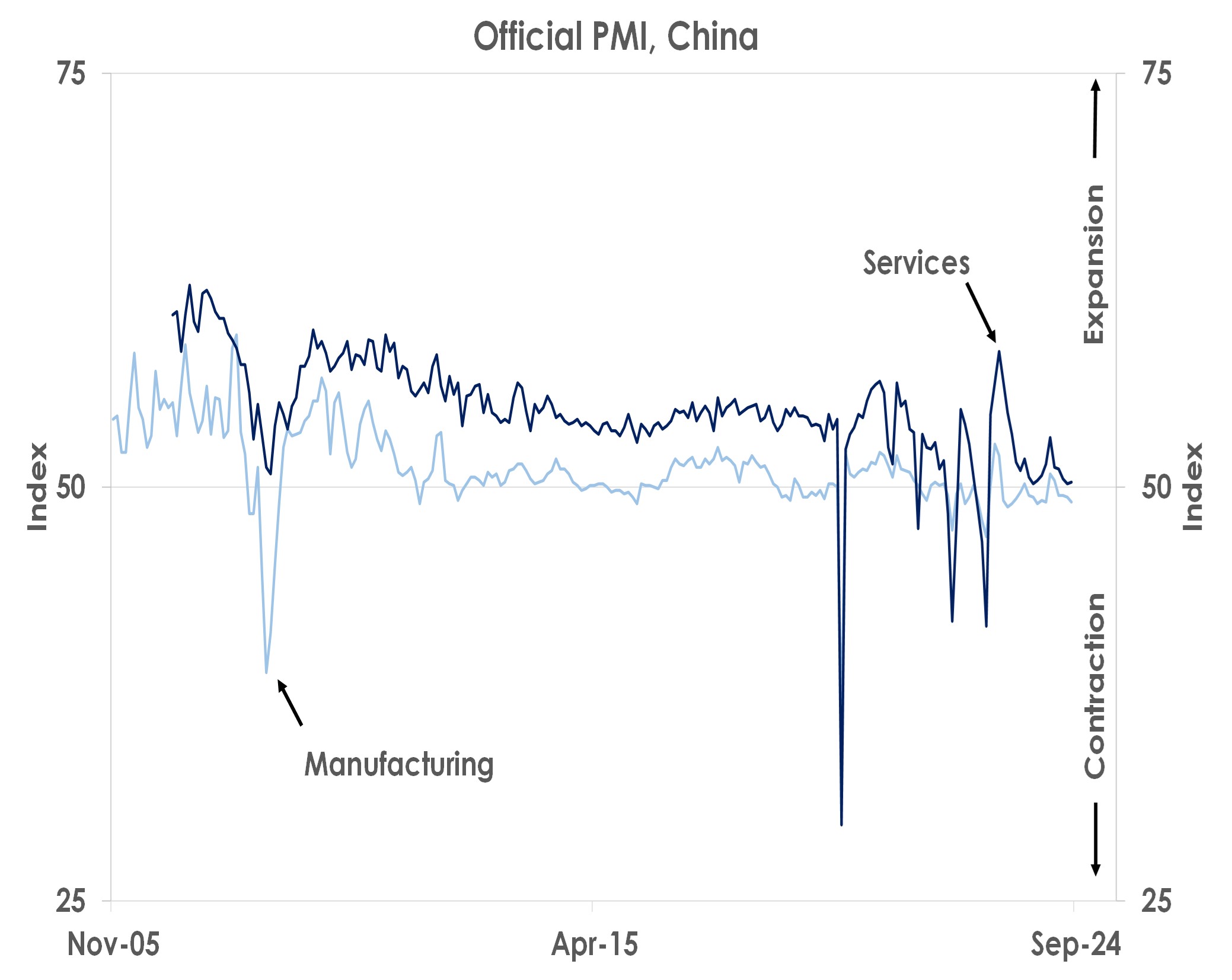

August’s PMIs show corporate confidence continues to be lacklustre in China.

Source: Bank of Singapore, Bloomberg

Troublingly, manufacturing PMI fell from 49.4 to 49.1 indicating activity contracted for the fourth month in a row. Bad weather affected the data. But the sector remains hobbled by weak demand.

August’s services PMI improved marginally from 50.2 to 50.3 - above the survey’s key 50.0 level that separates expansion from contraction - but overall demand in the sector stayed subdued. In contrast, when China fully reopened from the pandemic at the start of 2023, services PMI exceeded 58.0 as the chart above illustrates.

Source: Bank of Singapore, Bloomberg

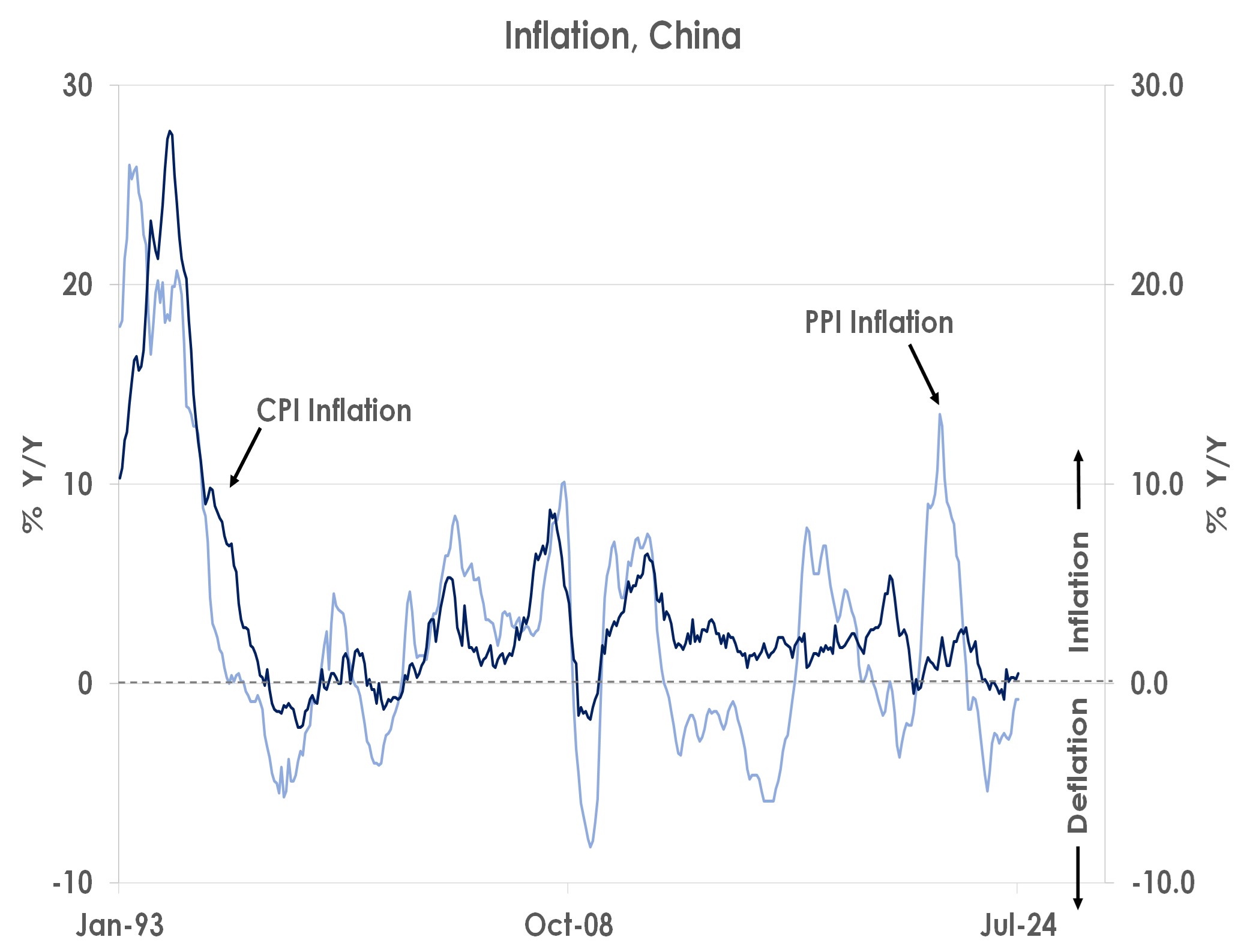

China’s halting recovery from the pandemic since lockdowns were lifted at the end of 2022 has kept inflation low, consumers cautious and property markets still fragile. The second chart shows consumer price index (CPI) inflation was just 0.5% in July.

Source: Bank of Singapore, Bloomberg

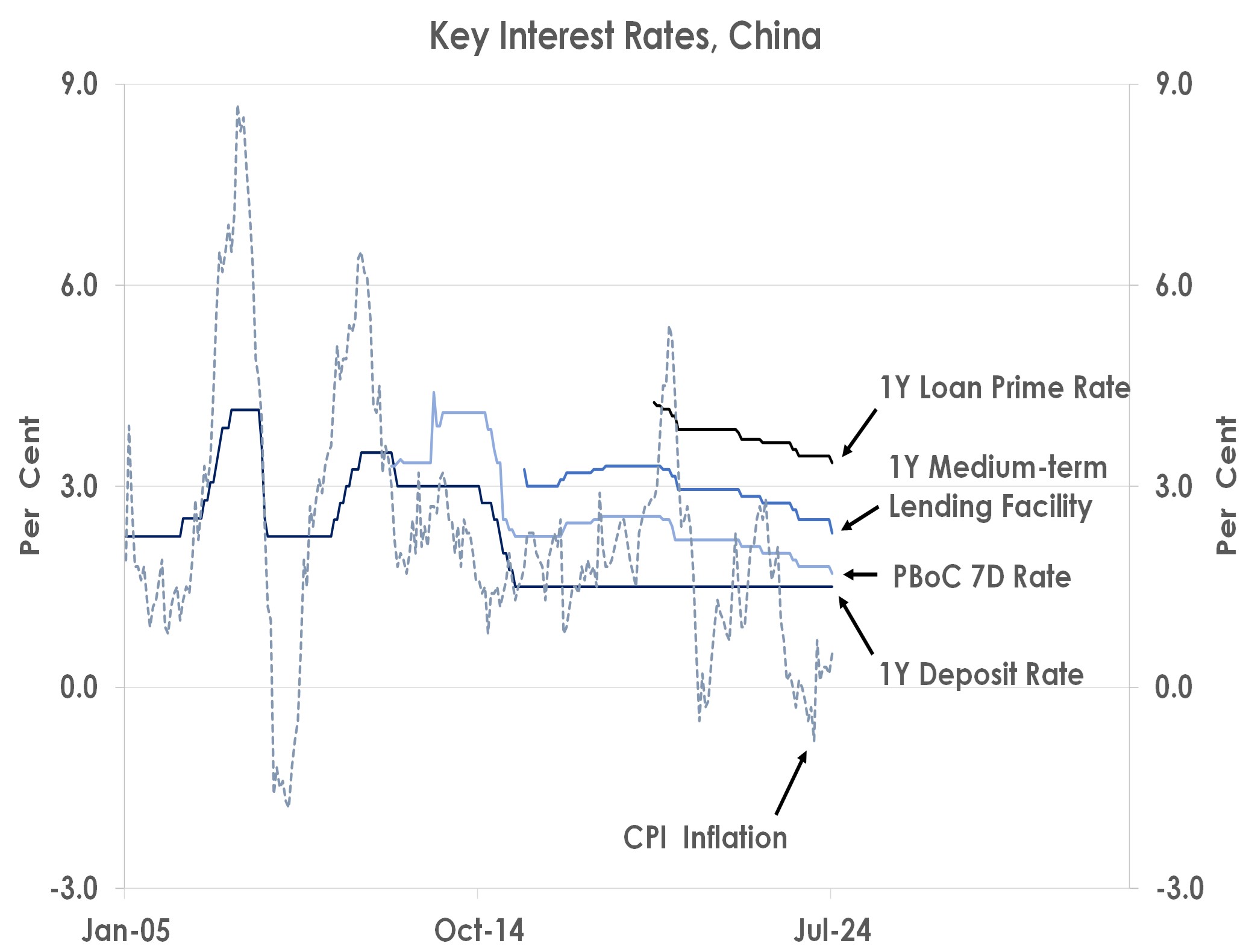

August’s PMI data indicate the current headwinds to growth in China are continuing. In response, the People’s Bank of China has already cut interest rates this year as the last chart shows and central and local governments are accelerating bond issuance to fund new investment. But with sentiment weak amongst firms and consumers, we think further rate cuts and fiscal stimulus will be needed to reach this year’s 5% GDP growth target and support China’s flagging financial markets.

Important information

This product may only be offered: (i) in Hong Kong, to qualified Private Banking Customers and Professional Investors (as defined under the Securities and Futures Ordinance); and (ii) in Singapore, to Accredited Investors (as defined under the Securities and Futures Act) and (iii) in the Dubai International Financial Center to Professional Clients (as defined under the Dubai Financial Services Authority rules) only. No other person should act on the contents of this document.This product may involve derivatives. Do NOT invest in it unless you fully understand and are willing to assume the risks associated with it. If you have any doubt, you should seek independent professional financial, tax and/or legal advice as you deem necessary.

Please carefully read and make sure that you understand all Risk Disclosures, Selling Restrictions, and Disclaimers. This document must be read together with the relevant Prospectus & Offering Documents &/or Key Fact Statement.

Disclaimer

The Bank, its Affiliates and their respective employees are not in the business of providing, and do not provide, tax, accounting or legal advice to any clients. The material contained herein is prepared for informational purposes and is not intended or written to be used, and cannot be used or relied upon for tax, accounting or legal advice. Any such client is responsible for consulting his/her own independent advisor as to the tax, accounting and legal consequences associated with his/her investments/transactions based on the client’s particular circumstances.

This document and other related documents have not been reviewed by, registered or lodged as a prospectus, information memorandum or profile statement with the Monetary Authority of Singapore nor any regulator in Hong Kong or elsewhere.

This document may not be published, circulated, reproduced or distributed in whole or in part to any other person without the Bank’s prior written consent. This document is not intended for distribution to, publication or use by any person in any jurisdiction outside Singapore, Hong Kong, or such other jurisdiction as the Bank may determine in its absolute discretion, where such distribution, publication or use would be contrary to applicable law or would subject the Bank and its related corporations, connected persons, associated persons and/or affiliates (collectively, “Affiliates”) to any registration, licensing or other requirements within such jurisdiction.