US Federal Reserve Chair, Jerome Powell. AFP.

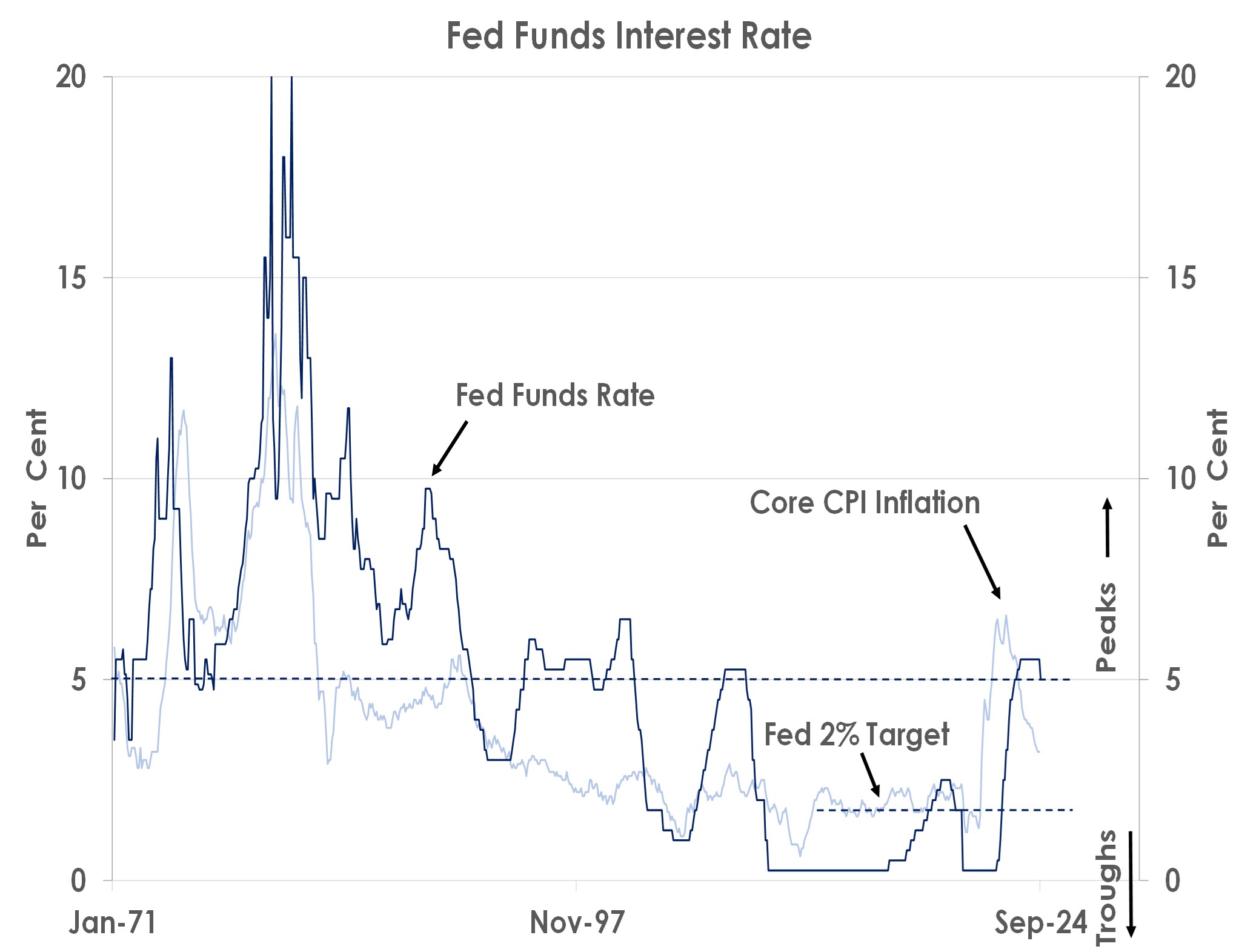

The Federal Reserve surprised by starting its interest rate cutting cycle with a 50bps reduction in the fed funds rate from 5.25-5.50% to 4.75-5.00% rather than with a 25bps move widely expected by investors.

Chairman Powell justified the decision by arguing it showed the Fed would not fall behind the curve as the US jobs market slowed: ‘the labour market is actually in solid condition, and our intention with our policy move today is to keep it there … we don’t think we’re behind. You can take this as a sign of our commitment not to get behind.’

The Fed Chair also said the 50bps rate cut reflected officials’ ‘confidence that inflation is coming down toward 2% on a sustainable basis.’

However, after first reacting positively to the larger-than-expected ate cut, the S&P 500 Index fell 0.3% overnight, gold ended lower too despite initially making a new all-time high of USD2,600, 10Y UST yields rose to 3.70% and the USD firmed to 143 against the JPY.

Financial markets fell as the Fed’s updated forecasts implied the fed funds rate would only be lowered in 25bps moves going forward.

The median projection from the Federal Open Market Committee (FOMC) showed the fed funds rate ending 2024 at 4.25-4.50%, and thus signalled two 25bps cuts in November and December. Similarly, the forecasts implied four 25bps cuts in 2025 and two in 2026 to lower the fed funds rate to 2.75-3.00%.

Source: Bank of Singapore, Bloomberg

The chart shows officials thus only projected the fed funds rate to gradually reach neutral levels near 3% over the next couple of years. We therefore think:

Important information

This product may only be offered: (i) in Hong Kong, to qualified Private Banking Customers and Professional Investors (as defined under the Securities and Futures Ordinance); and (ii) in Singapore, to Accredited Investors (as defined under the Securities and Futures Act) and (iii) in the Dubai International Financial Center to Professional Clients (as defined under the Dubai Financial Services Authority rules) only. No other person should act on the contents of this document.This product may involve derivatives. Do NOT invest in it unless you fully understand and are willing to assume the risks associated with it. If you have any doubt, you should seek independent professional financial, tax and/or legal advice as you deem necessary.

Please carefully read and make sure that you understand all Risk Disclosures, Selling Restrictions, and Disclaimers. This document must be read together with the relevant Prospectus & Offering Documents &/or Key Fact Statement.

Disclaimer

The Bank, its Affiliates and their respective employees are not in the business of providing, and do not provide, tax, accounting or legal advice to any clients. The material contained herein is prepared for informational purposes and is not intended or written to be used, and cannot be used or relied upon for tax, accounting or legal advice. Any such client is responsible for consulting his/her own independent advisor as to the tax, accounting and legal consequences associated with his/her investments/transactions based on the client’s particular circumstances.

This document and other related documents have not been reviewed by, registered or lodged as a prospectus, information memorandum or profile statement with the Monetary Authority of Singapore nor any regulator in Hong Kong or elsewhere.

This document may not be published, circulated, reproduced or distributed in whole or in part to any other person without the Bank’s prior written consent. This document is not intended for distribution to, publication or use by any person in any jurisdiction outside Singapore, Hong Kong, or such other jurisdiction as the Bank may determine in its absolute discretion, where such distribution, publication or use would be contrary to applicable law or would subject the Bank and its related corporations, connected persons, associated persons and/or affiliates (collectively, “Affiliates”) to any registration, licensing or other requirements within such jurisdiction.