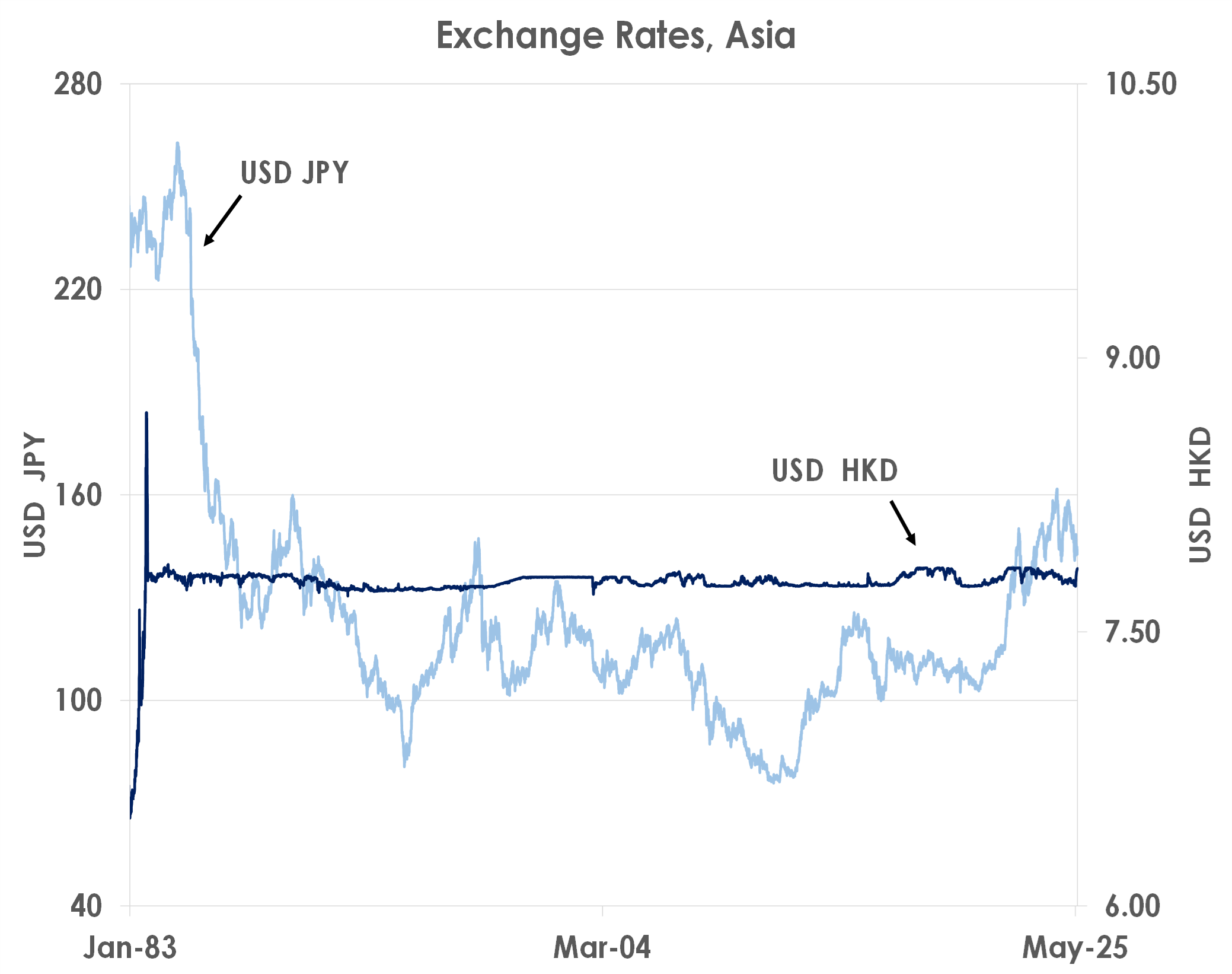

The Hong Kong Monetary Authority (HKMA) has pegged the HKD to the USD since 1983, most recently in a tight range of 7.75-7.85. The chart below shows the exchange rate has been stable while other currencies like the JPY have swung sharply over the last four decades.

Source: Bank of Singapore, Bloomberg

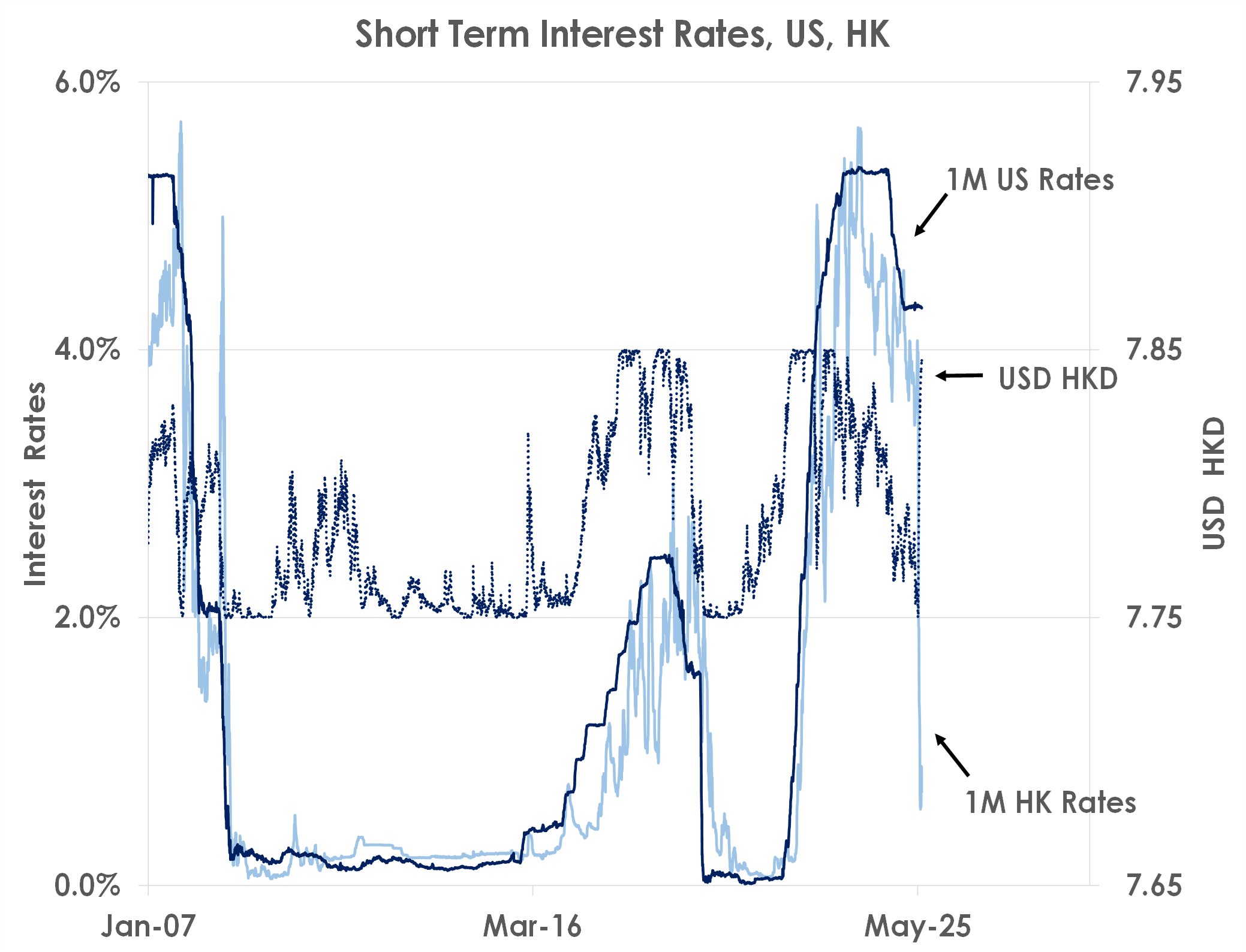

By tying its currency to the USD, the HKMA needs to ensure short-term HK interest rates are aligned with US rates and thus with the Federal Reserve’s policies. As the next chart shows, 1M HK interbank offered rates (HIBOR) have largely tracked 1M US secured overnight financing rates (SOFR). With interest rate differentials limited, traders have kept the HKD within its 7.75-7.85 range against the USD.

Source: Bank of Singapore, Bloomberg

This year the sharp weakness of the USD globally has put upward pressure on the HKD, pushing the currency to the strong side of its band at 7.75. The HKMA has responded by flooding domestic markets with liquidity, forcing HK interest rates down as the chart shows. Surprisingly, the HKMA action has resulted in HK rates falling more than 300bps below US rates – the widest divergence on record – causing the HKD to fall to the weak side of its band now at 7.85. This would usually cause the HKMA to respond by draining liquidity to push HK interest rates back up towards US rates to keep the HKD peg intact. But the HKMA hasn’t been forced to narrow the gap between HK and US interest rates. Instead, traders have been willing to hold HKD despite far lower HK rates due to concerns the HKMA could potentially surprise by loosening the band or even removing the peg. A sudden change would likely cause the HKD to surge given the USD’s current weakness globally.

We think investors should keep an eye on the HKD. The peg is most likely to stay in place as exchange rate stability supports Hong Kong as a financial centre. But any shift now would be a major surprise to global markets. In the current environment of volatile US assets, the USD would likely slide against the EUR and other major currencies, and US Treasury yields would spike on fears other central banks may abandon their USD pegs. Thus, a HKD shock in 2025 may hit global markets as much as the 2015 CHF shock – when the Swiss National Bank suddenly abandoned its exchange rate cap without warning.

Important information

This product may only be offered: (i) in Hong Kong, to qualified Private Banking Customers and Professional Investors (as defined under the Securities and Futures Ordinance); and (ii) in Singapore, to Accredited Investors (as defined under the Securities and Futures Act) and (iii) in the Dubai International Financial Center to Professional Clients (as defined under the Dubai Financial Services Authority rules) only. No other person should act on the contents of this document.This product may involve derivatives. Do NOT invest in it unless you fully understand and are willing to assume the risks associated with it. If you have any doubt, you should seek independent professional financial, tax and/or legal advice as you deem necessary.

Please carefully read and make sure that you understand all Risk Disclosures, Selling Restrictions, and Disclaimers. This document must be read together with the relevant Prospectus & Offering Documents &/or Key Fact Statement.

Disclaimer

The Bank, its Affiliates and their respective employees are not in the business of providing, and do not provide, tax, accounting or legal advice to any clients. The material contained herein is prepared for informational purposes and is not intended or written to be used, and cannot be used or relied upon for tax, accounting or legal advice. Any such client is responsible for consulting his/her own independent advisor as to the tax, accounting and legal consequences associated with his/her investments/transactions based on the client’s particular circumstances.

This document and other related documents have not been reviewed by, registered or lodged as a prospectus, information memorandum or profile statement with the Monetary Authority of Singapore nor any regulator in Hong Kong or elsewhere.

This document may not be published, circulated, reproduced or distributed in whole or in part to any other person without the Bank’s prior written consent. This document is not intended for distribution to, publication or use by any person in any jurisdiction outside Singapore, Hong Kong, or such other jurisdiction as the Bank may determine in its absolute discretion, where such distribution, publication or use would be contrary to applicable law or would subject the Bank and its related corporations, connected persons, associated persons and/or affiliates (collectively, “Affiliates”) to any registration, licensing or other requirements within such jurisdiction.